.jpg)

The short answer? Yes, you can absolutely rent out your condo. But that simple ‘yes’ comes with some pretty big ‘ifs’ that every aspiring landlord needs to get straight before putting up a "For Rent" sign.

Think of it less like a single decision and more like getting a series of green lights—first from your Homeowners Association (HOA), then from local authorities, and sometimes even from your mortgage company.

Renting your condo can be a fantastic way to generate income and build equity, especially when the rental market is hot. And it is. The real estate rental market is booming, with some analysts projecting its value to hit $3.87 trillion by 2029. This surge is largely driven by high home prices pushing more people to rent instead of buy. You can dig into more rental market trends with this detailed report.

But transforming your condo from a personal residence into a profitable rental property isn't as simple as just finding a tenant. It’s a journey that takes you from being a condo owner to becoming a compliant, successful landlord. You first have to work through a hierarchy of rules and responsibilities before you can even think about collecting rent.

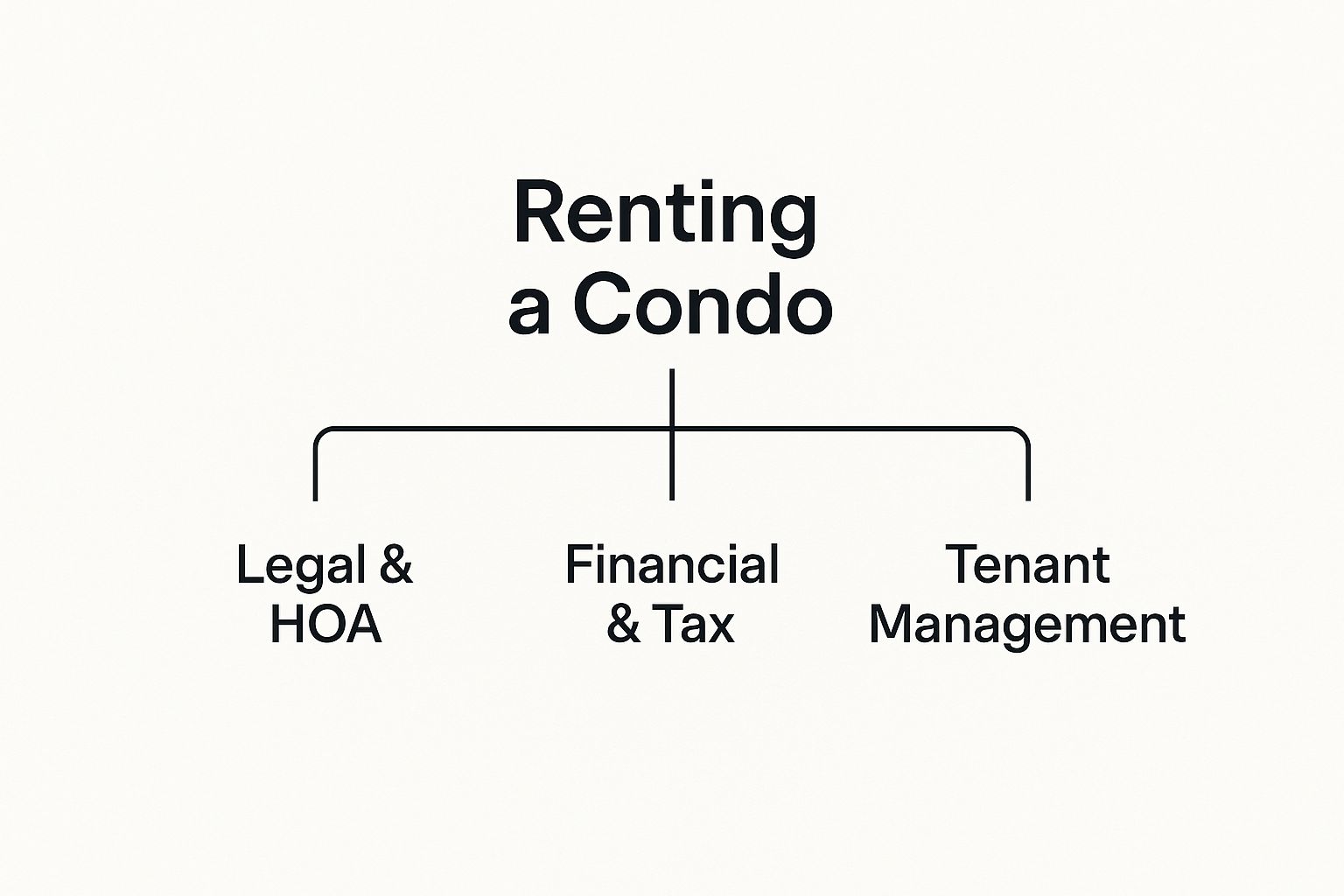

Understanding this pecking order of approvals is non-negotiable.

As you can see, successfully renting your condo means you're juggling legal, financial, and tenant-related duties all at once. Each of these areas has its own rulebook and its own set of challenges you'll need to master.

The biggest mistake new condo landlords make is assuming they can rent their unit just like a single-family home. In reality, your HOA's Covenants, Conditions, and Restrictions (CC&Rs) are your primary rulebook, and ignoring them can lead to hefty fines or legal action.

To get started on the right foot, you need a clear picture of the landscape. This means taking a few critical first steps.

Before you even start thinking about rental rates or tenant applications, it's essential to perform some initial due diligence. This checklist covers the absolute must-dos to determine if renting your condo is even a possibility.

Nailing down these "big ifs" from the get-go is what separates a smooth, profitable rental experience from a nightmare of fines and legal headaches. This guide will walk you through each of these steps, from decoding your HOA's bylaws to finding that perfect tenant.

Before you even start picturing rental income rolling in, there’s a crucial first stop: your Homeowners Association (HOA). Your HOA acts as the guardian of the community, and its main job is to protect everyone's property values. A big part of that mission involves setting firm rules around rentals.

These aren’t just friendly suggestions; they're legally binding regulations baked into a document called the Covenants, Conditions, and Restrictions (CC&Rs). Trust me, skipping over this document is the single biggest mistake a new condo landlord can make. Your CC&Rs are where you'll find out if you can even rent your condo and, if so, exactly what the process looks like.

Once you dive into your HOA’s governing documents, you'll probably run into a few key clauses meant to keep rental activity in check. These rules are there to help maintain a stable, owner-focused atmosphere in the community. Here’s what to look for:

While these restrictions can feel a bit restrictive, they are absolutely enforceable and are designed to protect the community’s long-term value. It’s also worth noting that these rules can sometimes connect to other financial duties, like when a board has to levy extra charges. Getting familiar with your community's policies on HOA special assessment rules can give you a more complete picture of what you're responsible for as an owner.

Let’s play this out. Imagine you've decided to rent out your condo. You found the perfect tenant, they passed the background check, and you’re all set to sign the lease. You send the paperwork over to your HOA, only to get a response that the community's 20% rental cap was hit months ago. You’re now number seven on the waiting list.

This isn’t just a hypothetical story; it’s a reality for a lot of condo owners. The big lesson here is to check the rental cap and get on that waiting list before you do anything else. Talking to your HOA board early and often is key.

In a situation like this, your first move should be to formally request to be added to the rental waiting list. Make sure you get confirmation in writing and ask where you are in the queue. After that, it’s a good idea to check in with the property manager or HOA board every so often to see where you stand. This proactive approach means that when a spot finally opens up, you’ll be ready to go without any frustrating delays.

Navigating your HOA’s rules is just the first hurdle. Once you get their approval, you step into the much bigger world of legal and financial duties that come with being a landlord. Answering the question "can you rent out a condo" with a confident "yes" means you need to start running your rental like a professional, business-minded operation from day one.

This requires a real shift in perspective. You're no longer just a condo owner; you're providing housing, which is a heavily regulated field. It’s entirely on you to understand and follow all the applicable landlord-tenant laws, which can vary wildly by state and even by city.

These laws are the rulebook for the entire landlord-tenant relationship, covering everything from the initial application to the day your tenant moves out. They exist to ensure fairness and protect the rights of both parties, so you can bet that ignoring them can land you in serious legal trouble.

Here are the big areas you need to get right:

Beyond your HOA's specific rules, you absolutely have to master this broader legal landscape. For instance, a simple guide to California landlord-tenant laws can give you critical insights into your responsibilities and your tenant's rights. At the same time, understanding the finer points of effective HOA rules enforcement helps you see how all these different layers of rules fit together.

Staying legally compliant is directly tied to protecting yourself financially. Two areas that new condo landlords often completely overlook are their insurance policy and their mortgage agreement.

Your standard homeowner’s insurance policy is not designed for rental properties. It will almost certainly not cover you if something goes wrong. If a tenant gets injured or a fire starts, you could be staring down a massive bill with zero coverage.

You absolutely need a dedicated landlord insurance policy. This specialized coverage protects your unit itself, provides liability protection if a tenant sues you, and can even cover lost rental income while you're making repairs after a covered event.

Finally, pull out your mortgage paperwork and look for an owner-occupancy clause. Many lenders, especially for FHA or VA loans, require you to actually live in the property for a certain period—usually at least one year. Renting it out before that time is up could be a direct violation of your loan terms, giving the lender the right to call the entire loan due immediately. Always, always check with your lender first.

So, you've gotten the green light to rent out your condo. The next big decision on your plate is figuring out how you want to rent it. This choice really comes down to a trade-off between stability and flexibility, and it will shape everything from your income and workload to the specific rules you’ll need to follow.

Think of it like choosing a vehicle for a road trip. A long-term lease is like a reliable sedan—it offers a steady, predictable ride with pretty low maintenance. A short-term rental, on the other hand, is more like a high-performance sports car. It has the potential for thrilling returns, but it demands constant attention and skilled handling to navigate the sharp turns.

Your decision should ultimately align with your financial goals, your condo's location, and just how much time you’re willing to put into being a landlord.

A long-term rental is the traditional route, where you sign a lease with a tenant for an extended period, usually a year. This strategy is the bedrock of landlording for a reason—it’s prized for its consistency and requires far less day-to-day management.

With one tenant locked in for a full year, you get a predictable monthly income stream. This makes it so much easier to budget for your mortgage, HOA fees, and other property expenses. The day-to-day workload is also significantly lighter; after the initial effort of finding and screening a great tenant, your main jobs are collecting rent and handling the occasional maintenance call. This makes it a fantastic option for owners who want a more passive income.

Short-term rentals, made famous by platforms like Airbnb and Vrbo, involve renting your condo for just a few days or weeks at a time. This approach can be incredibly profitable, especially if your condo is in a hot tourist spot or a busy city center. Nightly rates for short stays are much higher than the prorated daily rate of a long-term lease, giving you a much higher ceiling for potential income.

This model is part of a massive global trend. The short-term rental market saw a 9% increase in listings in just one year, all driven by traveler demand. You can find more insights into the booming short-term rental market here. But this higher reward definitely comes with a much higher workload.

Short-term rentals transform you from a landlord into a hospitality manager. You are responsible for constant cleaning, guest communication, booking management, and restocking supplies—a commitment that can feel like a part-time job.

Before you jump in, it’s smart to see how these two strategies stack up side-by-side.

Every condo owner's situation is different, so weighing the pros and cons of each rental model is a critical step. The table below breaks down the key differences to help you decide which path aligns best with your goals and lifestyle.

Ultimately, there's no single "right" answer. A long-term rental offers peace of mind and passive income, while a short-term rental provides the potential for higher earnings if you're willing to put in the work. Your choice will define your experience as a condo landlord.

Once you've gotten the green light from your HOA and sorted out the legal side, the real fun begins. Now it's time to shift your mindset from simply being an owner to thinking like a business operator. Getting your condo ready for the rental market is more than a quick tidy-up; it's about strategically preparing and marketing your property to attract the best possible tenants.

Your first job is to get the condo "rent-ready." This means tackling all those little maintenance items you might have been putting off—from a slowly dripping faucet to the scuff marks on the baseboards. A fresh coat of neutral-colored paint is one of the easiest ways to make the space feel clean, bright, and practically brand new. If you're looking to make a bigger splash, small, smart upgrades can go a long way. For some cost-effective ideas that will catch the eye of premium tenants, check out our guide on how to raise your property value.

Before you even think about listing it, a final, thorough walkthrough is a must. This detailed apartment inspection guide is a fantastic resource to make sure you don't miss a single thing.

With your condo looking its absolute best, it’s time to show it off. In today's market, high-quality photos aren't just a suggestion—they're a requirement. They are the single most important tool you have to grab a renter's attention as they scroll through listings. Pair those great photos with a compelling description that doesn't just list features but sells a lifestyle. Talk about the building's amenities, the coffee shop around the corner, or the amazing morning light in the living room.

The demand for well-kept condos is definitely there. In 2023 alone, there were over 2.4 million active short-term rental listings in the U.S., and the appetite for these properties keeps growing. While that number is for short-term stays, it points to a broader trend: people love condo living, which is great news for long-term landlords, too.

The most critical part of this entire process is tenant screening. A great tenant is worth their weight in gold—they pay on time and treat your property with respect. A bad one can turn your investment into a nightmare. Don't cut corners here.

A rock-solid screening process should always include these four pillars:

Putting in this work upfront is the best way to protect your investment and kick off a smooth, profitable relationship with your new tenant.

Let's be honest. Managing your own rental condo can quickly start to feel like a second job. It's the late-night calls about a leaky faucet or weekend plans getting completely derailed by a tenant issue. At some point, many landlords ask themselves a crucial question: is this really a passive investment, or did I just create more work for myself?

If that sounds familiar, it’s the perfect time to think about hiring a property management company.

Bringing in a professional manager isn’t just about offloading tasks; it’s a strategic business decision to get your time back and secure your peace of mind. It’s what transforms your rental from an active headache into a truly hands-off asset. Imagine just seeing a direct deposit hit your account each month while a dedicated pro handles absolutely everything else. That's the real value they bring to the table.

A good management company takes on the entire operational burden of your rental condo. Before you make the call, it’s worth understanding the work involved in managing an investment property so you can appreciate what you're handing over. Their duties are surprisingly extensive and cover every single stage of the rental cycle.

This comprehensive support ensures your investment is not just protected but also profitable, all without demanding your constant attention. Here's a look at what they typically cover:

The decision to hire a property manager often comes down to a simple cost-benefit analysis of your own time. What is an hour of your weekend worth? A professional manager's fee often pales in comparison to the value of the time and stress you save.

Ultimately, if you live far from your rental, simply lack the time to manage it effectively, or just want to enjoy the financial benefits without the operational grind, hiring a property management company is a smart move. It allows you to step back and finally enjoy the passive income you set out to create in the first place.

As you get closer to renting out your condo, a few final questions always seem to pop up. Let's tackle the most common ones we hear from new landlords so you can move forward without any lingering doubts.

Let's be blunt: renting your condo without getting the green light from your Homeowners Association is a terrible idea. It’s a gamble that almost never pays off, and the consequences can be severe.

Your HOA can start hitting you with substantial fines, which often pile up daily until you fix the situation. They also have the power to take you to court to enforce the community rules, sticking you with the bill for all the legal fees and court costs.

In the worst-case scenarios, the HOA can even place a lien on your condo for all those unpaid fines. The bottom line is simple: always, always read your CC&Rs and get that formal approval in hand before your tenant even thinks about moving in.

Yes, you definitely do. Your standard homeowner's policy won't cut it once you have a tenant. That policy is designed for when you live in the property, not for rental situations. You’ll need to switch over to a landlord insurance policy.

This isn't just a suggestion; it's essential protection. Here’s why:

Just remember, your landlord policy doesn't cover your tenant's belongings. They’ll need to get their own renter’s insurance for that, and it's a good idea to require it in your lease.

Absolutely. Most HOAs have the legal authority to either severely restrict or completely prohibit short-term rentals. You'll typically find these rules spelled out in the governing documents, and they exist to promote community safety and prevent the high turnover that comes with vacation rentals.

A very common restriction is a minimum lease term. This could be 30 days, six months, or even a full year. A rule like this immediately makes it impossible to list your property on platforms like Airbnb or Vrbo for weekend or weekly stays. Dig into your documents to check for any clauses on short-term letting.

Feeling like you're drowning in rules and red tape? Let the experts at Towne and Country Property Management take the weight off your shoulders. We can turn your condo into a truly passive, stress-free investment by handling everything from tricky HOA compliance to day-to-day tenant management. Learn more about our seamless property management solutions today.

.png)